[vc_row full_width=”stretch_row” parallax=”content-moving” css=”.vc_custom_1536894570551{padding-top: 150px !important;padding-bottom: 150px !important;background: #eaeaea url(http://www.silvercliffcapital.com/wp-content/uploads/2018/09/08-Silk-Road-darken-1.jpg?id=4717);background-position: center;background-repeat: no-repeat !important;background-size: cover !important;}”][vc_column][/vc_column][/vc_row][vc_row parallax=”content-moving” css=”.vc_custom_1536800510804{background-position: center;background-repeat: no-repeat !important;background-size: cover !important;border-radius: 4px !important;}”][vc_column][vc_column_text]

Note: An edited version of this article was first published by Silvercliff Capital Partner Shiwen Yap in Venture Views on 27.07.2018

[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][vc_column_text]

With Singapore strengthening and deepening its involvement in China’s Belt and Road Initiative (BRI), a geo-economic infrastructure initiative that has emerged as a focal point in relations between the city-state and China, to what extent does China’s substantial corporate debt burden and its possible collapse pose a risk to the capital markets of the city-state?

Ying Khuan Pow, a Research Analyst with Knight Frank Asia Pacific, commented: “Although Singapore does not have any major BRI-related infrastructure projects on its shores, the fact remains that not only has Singapore the required synergy and connectivity with China and the other BRI countries, but it is also armed with an unprecedented depth of resources and expertise to facilitate the continuous development of BRI, including masterplanning, logistics and financing.”

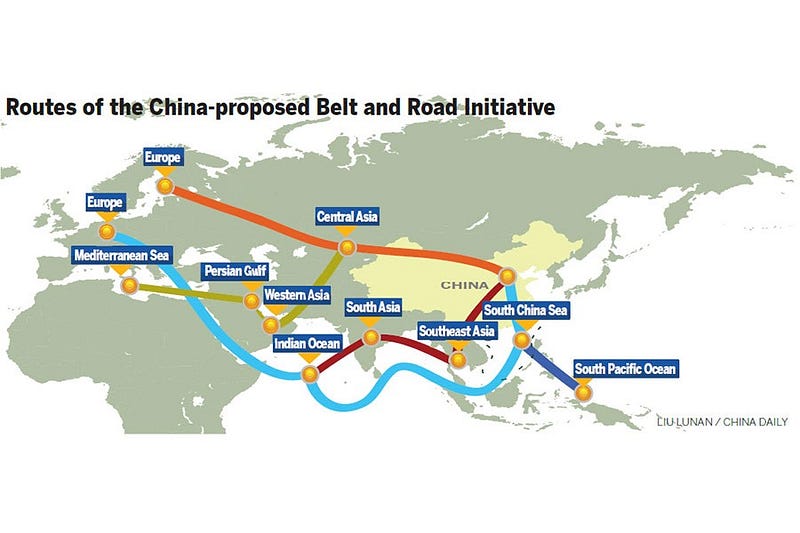

The BRI, which is envisaged to connect some 65 countries and nearly 60% of the global population across Eurasia and the Indo-Asia Pacific (Indo-APAC) region, has total investments at maturity are estimated at US$4 trillion. However, it has also generated criticism and stoked calls for a change in its narrative, particularly if China wishes benefit from the economic and political dividends.

While the BRI lays a foundation for China to potentially become the largest commercial empire in the world, there are also the possibilities of the mega-project failing to achieve its lofty goals of connecting the markets of Eurasia and East Africa, bringing them into the economic orbit of China.

One major risk that could impact the BRI’s success is China’s ageing society; it’s low birth rate and longer lifespans translates to about 25% of its population being over 65 years of age by 2050, with fewer young people to support them.

In a 2016 SCMP feature, Tom Holland, a veteran business journalist whose background includes stints at the Wall Street Journal, and CNBC, compared it to a similar plan rolled out by the late Japanese prime minister, Keizo Obuchi, in the 1990s which was designed to “provide work for Japan’s recession-hit construction sector” by building out Japanese-funded infrastructure projects around Asia.

Holland highlighted that while Asia requires additional infrastructure development, its capacity to absorb new projects is limited, with infrastructure projects that are economically viable being questionable. Holland argues that this could see Beijing “…building white elephants, wasting money, and encouraging corruption on a scale never before seen”.

This is coupled with recent reports of Chinese-backed state enterprises lagging in their performance, with their efficiency plummeting over the last decade, as well as claims that Chinese geostrategic ambitions may have trumped financial logic in the case of Sri Lanka.

Yet, a deeper analysis of Sri Lanka’s debt trap also highlights that political actors in these countries are also complicit in such situations, using Chinese funds to “service domestic political agendas and mitigate policy pressure from Western counterparts”

Despite these other factors at play, a forecast from global real estate consultant Knight Frank predicts China’s BRI will succeed, with a Knight Frank report published earlier this year noting that Singapore, alongside small states such as Qatar and the UAE, play a key role at this stage in the BRI’s development and stand to benefit from its involvement.

Capital Market Risks

There are a number of risk factors to Singapore, rooted in the development of a deeper economic connection to China — it emerged as China’s largest investor in 2015 and is a major destination for Chinese investment — meaning that China’s debt bubble bursting would adversely impact the city-state’s economy.

China is Singapore’s top trading partner, with bilateral trade amounting to S$137.1 billion in 2017. Since 2009, the value of exports exceeds imports for Singapore’s merchandise trade with China.

However, China has also financed a number of ports around Indo-APAC that could threaten Singapore’s primacy as a maritime centre, with Shanghai set to emerge as a major competitor to the city-state. Chinese investors are backing the development of a shipping centre in Malacca set to rival Singapore, with predictions that it will impact Singapore’s shipping sector thought the city-state maintains a competitive edge on its neighbour for the time being.

The BRI already faces a number of issues, with the project representing an attempt to combine economic and political diplomacy that exceeds the US Marshall Plan — which infused an estimated $13 billion ($135 billion in 2018) into rebuiling Europe — in scope and size.

Currently, it is financed by the $40 billion Silk Road Fund, which is backed by the China Investment Corporation (CIC), China’s three policy development banks and the State Administration for Foreign Exchange.

These banks will grant additional loans, with the People’s Bank of China having transferred $82 billion of additional capital, as well as the China-sponsored Asian Infrastructure Investment Bank. However, financing these ambitions is expected to take $5 trillion for the 2017–2022 period, with the source of these funds being unclear.

Beyond the economic dimension, other risks that emerge from BRI involvement include geopolitical and financial factors, as in the case of Sri Lanka and even Pakistan, a strategic ally of China and its counterweight to India. However, the debtbook diplomacy approach that China has adopted may generate strategic gains despite the financial losses incurred.

Commenting on the risk to capital markets, Dr Ernest Kan, Deputy Managing Partner, Deloitte Singapore and Board Member of the Deloitte Global Chinese Services Group, argues: “The Belt & Road initiative can help improve the circulation of resources, market integration and allow for better facilitation of trade and investment within Southeast Asia.”

“It is crucial that Singapore leverages its strengths as a global centre of trade, finance and talent as well as its geographical proximity and strong ties with China and Southeast Asia to tap growth opportunities arising from the Belt & Road trade routes.“

“Notwithstanding the concerns around the debt bubble, managing the multilateral ties and existing agreements will be critical for success, as it involves many countries. Chinese companies operating abroad will face a series of challenges consequent to the enactment of this initiative. As companies expand their global operations, there would be a rise in the risk of disruption in a particular country, affecting quality control or working capital issues.”

He adds, “Credit risk would be the next concern. The increase in cross-border activities will likely see a rise in uncertainties relating to trade embargos and infrastructure impediment, especially amongst the developing nations. Countries along the Belt and Road would then have to consciously work together to prevent such risks.”

“Having said that, the capital markets are not solely reliant on BRI’s development. Thailand, Indonesia and Singapore have shown strong performance with funds raised on the rise in the past four years.

Meanwhile, Dr Steven Matthew Oliver, Assistant Professor of Social Sciences (Political Science) at Yale-NUS in Singapore, whose research focus in the fields of comparative politics and international relations is on East Asia, notes: “To the degree that Singapore gets involved in BRI (presumably by helping to finance projects), it certainly faces the problem of getting stiffed if debtors cannot repay the loans.”

“Given the willingness of China to invest in projects where the return is uncertain (and the returns might instead be in terms of political returns to China rather than financial returns), partnering up to finance projects exposes Singapore to the risk of getting stuck with some of the bill (or part of an unused airport in the middle of nowhere).”

“If the Chinese debt issue comes to a head, then Singapore has problems whether or not it is involved in BRI. Certainly, greater involvement in the BRI would increase exposure. But the effects of the collapse of the Chinese debt bubble would be problematic for Singapore regardless,“ he adds.

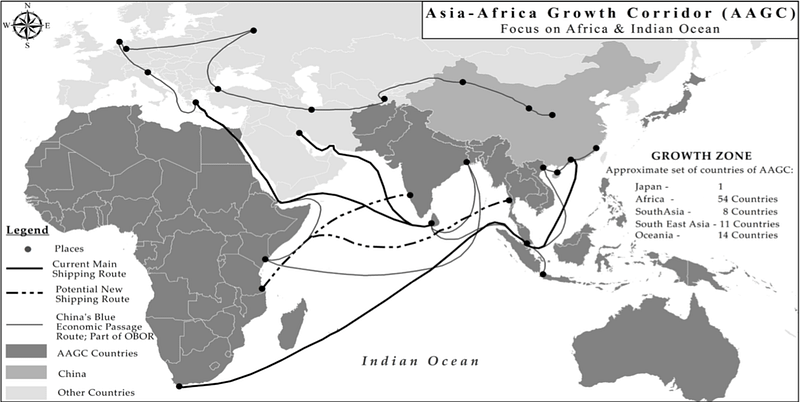

Asia-Africa Growth Corridor: An Alternative?

With Singapore tending to be perceived as a neutral destination — the June 2018 summit between US President Donald Trump and North Korean strongman Kim Jong Un highlights this political neutrality — a possible alternative to the BRI exists in the form of the Asia-Africa Growth Corridor (AAGC), a geo-economic initiative backed by Japan and India.

According to details in a report by India’s Centre for Air Power Studies, as of June 2017 Japan has already invested an estimated $32 billion in African infrastructure projects, with $200 billion committed to the AAGC. India, which posted trade with Africa of approximately $72 billion in the 2014/2015 period, is still firming up its own investment plans for the AAGC. India-Africa trade for 2018 is forecast to reach $100 billion.

Asked if the AAGC offers a clear alternative to the BRI with an approach that is reportedly more open and inclusive, Dr Oliver observed: “What seems to differentiate the AAGC from the BRI is the bilateral nature of much of BRI versus the (potential for a more) multilateral approach in the AAGC.”

“Although China has set up multilateral institutions like the AIIB for funding BRI projects, most of the initiative (e.g. financing) is still done on a bilateral basis (e.g. Chinese state-owned banks or funds doing most of the financing). China prefers to do conduct its business on a bilateral basis as it allows it to throw its weight around and get its own way without the intrusion of other states, international organisations, etc. Territorial disputes in the South China Sea and China’s desire to resolve all such disputes are a case in point.”

He adds, “Bilateralism is an issue for small states who would instead prefer multilateral arrangement that provide more channels for small states to manoeuvre, link issues with other parties, and get what they want. That said, it is not yet clear that AAGC offers a clear alternative in that it remains (as I understand it) a largely bilateral initiative between India and Japan. It just seems to have more potential than BRI.”

Regardless of whether the BRI succeeds or fails — a Financial Times editorialargues that it could export the worst of China’s economy while increasing the strain on its financial infrastructure — Dr Kan opined in an interview with Deal Street Asia that BRI developments in Southeast Asia will be successful, with the bamboo network of Chinese-owned enterprises in the region benefiting greatly from it.

Dr Kan explains: “BRI developments open up opportunities for all Chinese enterprises. Privately-owned Chinese family businesses can benefit from the spillover effects of the infrastructure projects mostly delivered by State-owned Enterprises (SOEs).”

He also argues that Singapore itself will benefit greatly from its involvement in financing developments across the region. He observes: “Considering Singapore’s strong roots as a regional trading and financial hub, Singapore would benefit from participating in the co-creation of the BRI by adopting active roles in key areas such as transport, finance, trade, telecom infrastructure and resources.”

Moreover, the AAGC has the potential to become part of a broader infrastructure initiative by the US, Japan, India and Australia to counter the BRI and China’s growing influence, thought such plans are still nascent.

BRI & AAGC Synergies?

Given Singapore’s position as a neutral venue and its potential as an Indo-Asia Pacific (Indo-APAC) super-connector — comparable to Hong Kong’s own role as a super-connector for China — it must be borne in mind that Japan’s own backing of the BRI is aimed at shaping China into a “responsible global player”.

Since 2016, Singapore has deepened its ties with Japan and strengthened its relationship with India, as part of its long-standing policy of engaging all major powers with a presence in Southeast Asia and the wider Indo-APAC region.

Concurrently, Singapore is also the largest offshore hub in Asia for RMB trading outside Hong Kong and the fifth globally, accounting for 5% of all renminbi trades globally in April 2017 and ranking alongside London as a major centre by 2030. This translates to the city-state having the potential to leverage this these relationships in order to generate synergies between the AAGC and BRI.

However, one research note highlights that while Japan and India enjoy robust social momentum in Africa relative to China, the “Chinese pattern of investment and economic diplomacy seems to be at present paramount”, with China currently better positioned to implement BRI projects and with a momentum advantage in collaborating with developing countries in Asia and Africa, as well as favourable perceptions of Chinese economic diplomacy.

The only viable way to surmount the BRI then is to create a mechanism that includes African stakeholders through a common institution that can “monitor the timely completion of projects and also ensure quality control”, which is where China’s BRI lags.

Dr Oliver notes: “A priori there does not appear that the two initiatives cannot be made to complement one another. Although credible commitment is a potential concern (i.e. can China or Japan-India credibly commit not to exclude the other or use its investments to harm their interests), the fact that commitment is a potential concern does not mean that arrangements cannot be made of address issue.”

Weighing in on the matter, Dr Kan observes: “Singapore is an open economy with a multi-pronged approach to foreign affairs and economic policies. Besides the BRI and AAGC, Singapore is also actively involved in the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP), and have tax treaties and MOUs with several countries.”

Noting that the city-state maintains “competitive advantages as the leading clean energy hub” for Southeast Asia, Dr Kan argues that this has attracted foreign businesses from Indonesia and Japan to adopt Singapore as a reference market for testing their products and services prior to expansion into neighbouring regional countries.

Adding that its strength as a global financial centre with a “strong network of financial institutions with excellent governance” has drawn firms to Singapore to pursue fundraising activities, Dr Kan expects the BRI to “further increase the opportunities for professional services firms in Singapore to raise and distribute equity and debt capital” that will facilitate further investment around Southeast Asia.

With Singapore seeking deeper business ties in Africa’s emerging markets, it could leverage elements of its international branding in Africa, as well as to explore ways through which it could serve as a platform to merge these two competing geo-economic initiatives. Such a move could leverage its established neutrality, as well as augment its current position as the Chair of ASEAN.

Additionally, doing so would enhance the development of its external economy, whose development has been driven by global macroeconomic trends.

The strength of this external economy is measure by the robust growth in Export of Goods, Export of Services and Direct Investment Abroad (DIA) by Singapore-based companies, with its stock of DIA growing by a multiple of 25X from S$17 billion in S$426 billion between 1990 and 2010.

Given these various factors at play, it is in Singapore’s economic self-interest to explore supporting both initiatives and bridging both the AAGC and BRI through a single platform; beyond being aligned with existing core principles of its foreign policy, it also mitigates the risk that can come from shocks in the capital markets of China, the US and neighbouring nations.

[/vc_column_text][/vc_column][/vc_row][vc_row][vc_column][vc_row_inner css=”.vc_custom_1536662682945{margin-top: 100px !important;}”][vc_column_inner width=”1/3″][vc_custom_heading text=”WEBSITE:” font_container=”tag:p|font_size:14|text_align:left” use_theme_fonts=”yes” link=”|||”][vc_custom_heading text=”Home” font_container=”tag:p|font_size:14|text_align:left” use_theme_fonts=”yes” link=”url:http%3A%2F%2Fsilvercliffcapital.com%2Findex.php%2Fteam%2F|||”][vc_custom_heading text=”Team” font_container=”tag:p|font_size:14|text_align:left” use_theme_fonts=”yes” link=”url:http%3A%2F%2Fsilvercliffcapital.com%2Findex.php%2Fteam%2F|||” css=”.vc_custom_1536661465470{margin-top: -15px !important;}”][vc_custom_heading text=”News and views” font_container=”tag:p|font_size:14|text_align:left” use_theme_fonts=”yes” css=”.vc_custom_1536661472267{margin-top: -15px !important;}”][vc_custom_heading text=”Contacts” font_container=”tag:p|font_size:14|text_align:left” use_theme_fonts=”yes” css=”.vc_custom_1536662919632{margin-top: -15px !important;}”][/vc_column_inner][vc_column_inner width=”1/3″][vc_custom_heading text=”OUR ADDRESS:” font_container=”tag:p|font_size:14|text_align:left” use_theme_fonts=”yes”][vc_custom_heading text=”03-01, 8 Claymore Hill, Singapore, 229572″ font_container=”tag:p|font_size:14|text_align:left” use_theme_fonts=”yes” link=”url:https%3A%2F%2Fgoo.gl%2Fmaps%2FD1fKZzw37zj|||”][/vc_column_inner][vc_column_inner width=”1/3″][vc_custom_heading text=”FOLLOW US:” font_container=”tag:p|font_size:14|text_align:left” use_theme_fonts=”yes”][vc_custom_heading text=”LinkedIn” font_container=”tag:p|font_size:14|text_align:left” use_theme_fonts=”yes” link=”url:https%3A%2F%2Fwww.linkedin.com%2Fcompany%2Fsilvercliffcapital%2F|||”][/vc_column_inner][/vc_row_inner][vc_row_inner][vc_column_inner css=”.vc_custom_1536668899487{margin-top: 50px !important;}”][vc_custom_heading text=”@2018 Silvercliff Capital Advisors LLP. All rights reserved” font_container=”tag:p|font_size:14|text_align:left” use_theme_fonts=”yes”][/vc_column_inner][/vc_row_inner][/vc_column][/vc_row]

25 Comments